Churches, like any other organization, need to keep a close eye on their finances to ensure a stable future and continued growth. We’ll explore the unique intricacies of church accounting and offer practical guidance to help faith-based organizations navigate their financial journey.

By understanding what sets church accounting apart from conventional methods, your organization can achieve both spiritual and financial success.

How is Church Accounting Different?

Church accounting stands apart from accounting in other organizations for various reasons, including the adoption of fund accounting, the unique revenue streams, the emphasis on mission over profits, and certain regulatory obligations.

Fund Accounting

Fund accounting is a specialized branch of accounting designed to track and manage the financial activities of non-profit organizations, including churches. Unlike traditional accounting methods, fund accounting emphasizes accountability and transparency, ensuring that funds are allocated and utilized for their intended purposes.

By segregating financial resources into separate accounts, or “funds,” this system enables organizations to closely monitor and report on the performance of each fund. As a result, fund accounting plays a crucial role in maintaining the trust of donors, stakeholders, and regulatory bodies by providing a clear and accurate picture of an organization’s financial health.

Nature of Revenue Sources

Churches use a variety of revenue sources to promote their mission, with a significant portion coming from the kindness of their congregations and community support.

Churches may obtain funding through:

- Tithes and offerings

- Sporadic donations

- Pledge campaigns

- Fundraising events and initiatives

- Grants

- Capital drives

- Investments

Each revenue stream revolves around voluntary contributions from their congregation and supporters. Sometimes, these sources have specific conditions, requiring the funds to be used for certain activities. For example, grant money could be designated for a scholarship program.

These requirements determine how church finances are allocated into specific “funds” within their financial systems. That’s why fund accounting is essential for churches, as it ensures compliance with and respect for these limitations.

Mission over Profits

The church accounting system is centered on advancing the mission and objectives of the church rather than generating profits. Financial resources are reinvested back into the organization to support its goals, such as outreach programs, community support, and spiritual growth. This focus contrasts with for-profit entities, where the primary objective is to maximize profitability and shareholder value.

Specific Regulatory Requirements

As 501(C)(3) entities in the US, churches are subject to specific regulatory requirements that differentiate their accounting practices from other organizations. Churches must adhere to the Generally Accepted Accounting Principles (GAAP) for various documents and reports and comply with IRS regulations. They must maintain accurate financial records, submit annual information returns, and ensure that their activities align with their tax-exempt status.

On the other hand, nonprofit organizations in Canada must adhere to specific accounting regulations, including the Canadian Accounting Standards for Not-for-Profit Organizations (ASNPO), which provide guidelines for financial reporting and disclosures. These organizations must also maintain accurate records, file annual information returns with the Canada Revenue Agency (CRA), and ensure proper handling of restricted funds. Compliance with these regulations ensures transparency, accountability, and proper financial management within the sector.

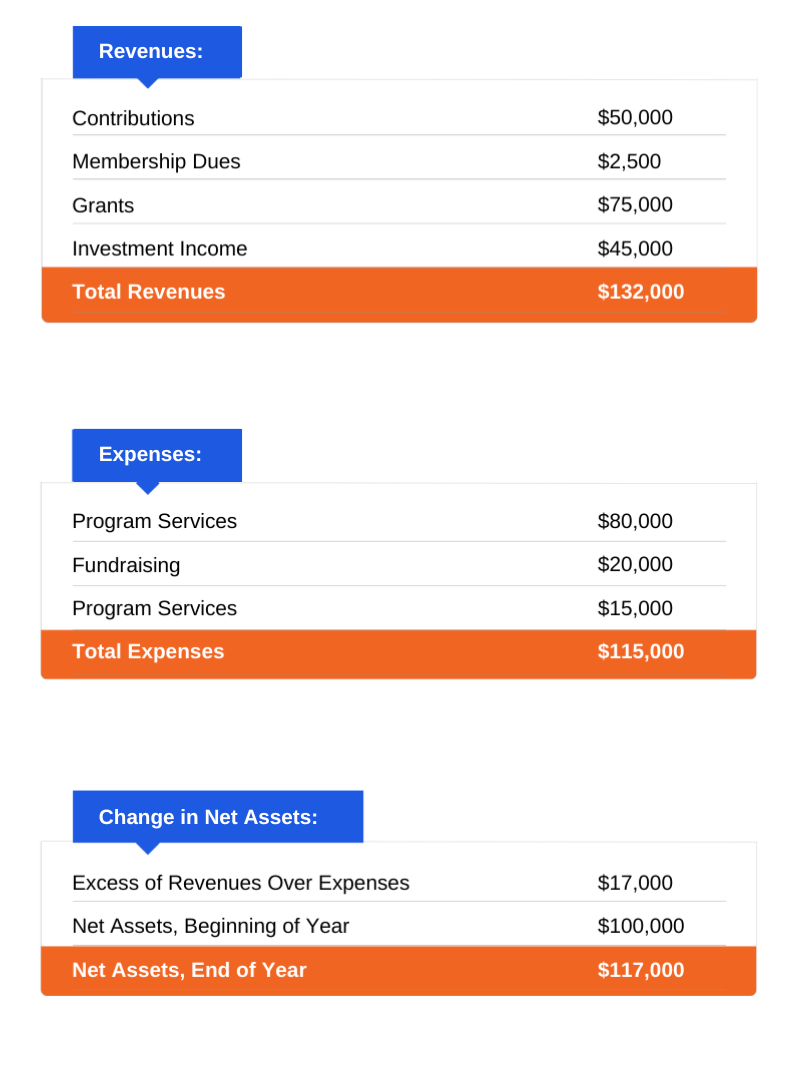

Statement of Activities

The Statement of Activities, also known as Income Statement is a crucial financial report for nonprofit organizations, such as churches, that offers a comprehensive view of the organization’s financial performance during a specific accounting period (usually a fiscal year). It focuses on the organization’s revenues, expenses, and the net change in its assets over that period. The primary purpose of this report is to provide a transparent and detailed overview of an organization’s financial activities, emphasizing how they align with the mission and objectives.

Key Components of the Statement of Activities:

- Revenues: The statement of activities lists all the revenue sources for the organization during the accounting period. Revenue sources for churches and nonprofits typically include donations, grants, tithes, offerings, pledge campaigns, fundraising events, and investment income. Revenues are often categorized as either unrestricted, temporarily restricted, or permanently restricted based on donor-imposed restrictions or stipulations.

- Expenses: The statement also outlines all the expenses incurred by the organization during the accounting period. These expenses may be related to program services, administration, or fundraising. To enhance transparency, expenses are usually classified by their function, such as salaries, rent, utilities, and supplies.

- Net Assets: The statement of activities calculates the net change in assets by subtracting total expenses from total revenues. This result helps stakeholders assess the organization’s financial health and its capacity to fulfill its mission and objectives.

Here’s an example of a Statement of Activities for a church.

Statement of Activities vs For-Profit Organization’s Income Statement

- Purpose: While the income statement focuses on a company’s profitability, the statement of activities emphasizes financial accountability and transparency in line with the organization’s mission and goals.

- Terminology: In the income statement, terms like “revenues,” “expenses,” and “net income” are used, while the statement of activities uses terms like “support,” “revenues,” “expenses,” and “change in net assets.”

- Focus on a mission: The income statement is designed to provide insight into a company’s financial performance and profitability, while the statement of activities focuses on illustrating how an organization’s financial resources are utilized to support its mission and objectives.

The statement of activities is a vital financial report for a non-profit organization that offers a comprehensive view of its financial performance. It differs from the income statement used by for-profit businesses, with a focus on financial accountability, transparency, and alignment with the organization’s mission and objectives.

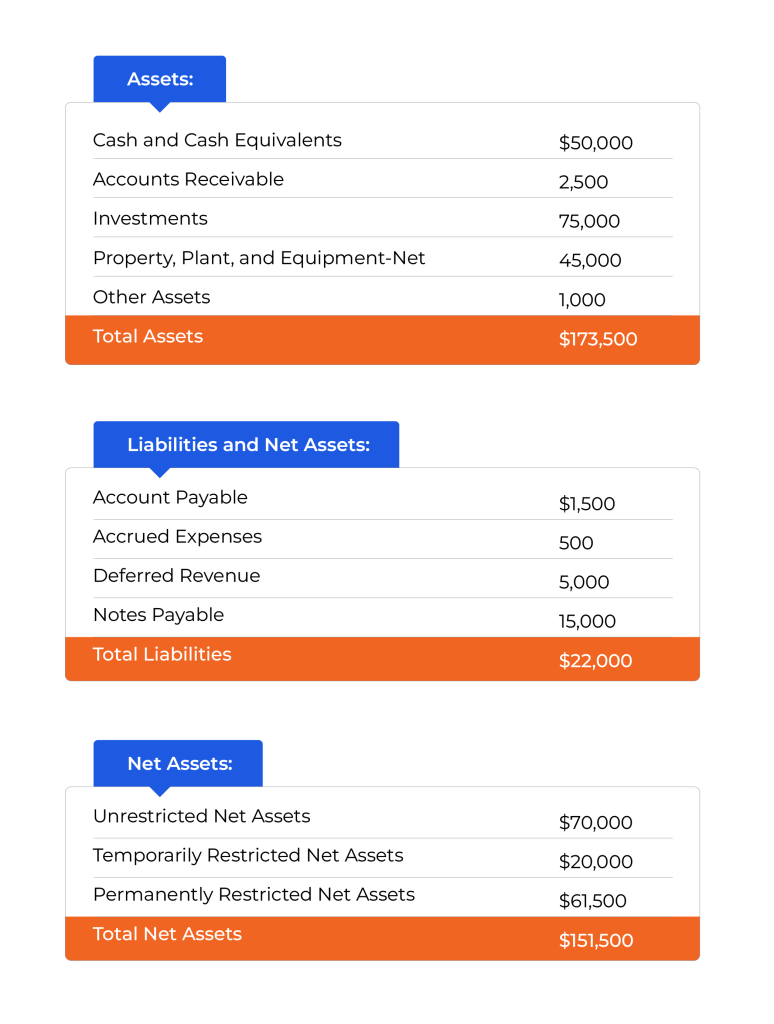

Statement of Financial Position

The Statement of Financial Position, also known as the Balance Sheet, is a fundamental financial report for nonprofit entities such as churches. It provides a snapshot of an organization’s financial health at a specific point in time by presenting its assets, liabilities, and net assets. The primary purpose of the Statement of Financial Position is to offer a comprehensive and transparent overview of an organization’s financial resources and obligations, allowing stakeholders to assess its financial stability and capacity to fulfill its mission and objectives.

Key Components of the Statement of Financial Position:

Assets

These represent the resources owned or controlled by the organization, such as cash, accounts receivable, inventory, investments, property, and equipment. The Statement of Financial Position lists the organization’s assets in order of liquidity, with the most liquid assets appearing first.

Liabilities

Liabilities are the obligations or debts that the organization owes to others, such as accounts payable, loans, and deferred revenue. Similar to assets, liabilities are listed in the order they are expected to be settled, with current liabilities appearing first.

Net Assets

Net assets represent the residual interest in an organization’s assets after deducting its liabilities. They are an indicator of the organization’s financial health and its ability to support its mission and objectives. Nonprofit organizations typically classify net assets into three categories: unrestricted, temporarily restricted, and permanently restricted. Unrestricted net assets have no donor-imposed restrictions, while temporarily and permanently restricted net assets have specific conditions set by the donor regarding their use or time frame.

Here’s an example of a Statement of Financial Position for a church.

Benefits of the Statement of Financial Position

- Financial Health Assessment: The Statement of Financial Position enables stakeholders to evaluate an organization’s financial stability, liquidity, and solvency. By analyzing the composition and relationship between assets, liabilities, and net assets, stakeholders can gauge the organization’s capacity to meet its obligations and support its mission.

- Decision-making: The statement serves as a valuable tool for the church administrators and board members, helping them make informed decisions about resource allocation, budgeting, and strategic planning. It also helps in identifying trends, potential risks, and areas for improvement.

- Accountability: The Statement of Financial Position demonstrates an organization’s commitment to financial accountability and transparency, allowing stakeholders to understand its financial resources and obligations.

- Compliance: Nonprofit organizations are required to present a Statement of Financial Position under the Generally Accepted Accounting Principles (GAAP) and the Financial Accounting Standards Board (FASB) guidelines.

The Statement of Financial Position is a vital financial report for nonprofit organizations that offers a comprehensive view of their financial health at a specific point in time. It highlights the organization’s assets, liabilities, and net assets, contributing to financial transparency, accountability, and informed decision-making, all of which are essential to the organization’s overall financial management and mission fulfillment.

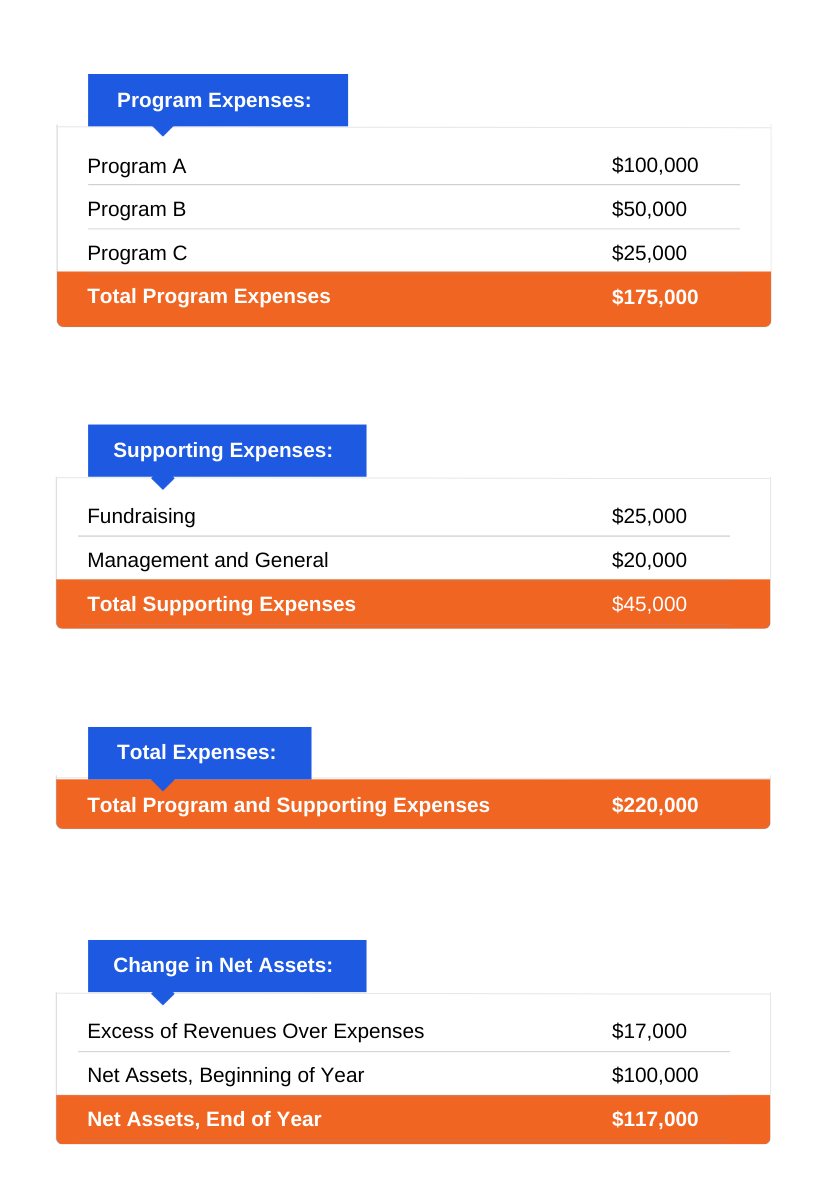

Statement of Functional Expenses

The Statement of Functional Expenses is an essential financial report for nonprofit accounting. This statement offers a detailed breakdown of an organization’s expenses by function and nature during a specific accounting period, usually a fiscal year. The primary objective of the Statement of Functional Expenses is to provide a transparent and comprehensive view of how an organization allocates its resources across various programs, administrative tasks, and fundraising activities.

Key Components of the Statement of Functional Expenses:

- Functional Categories: The statement organizes expenses into three primary functional categories: program services, management and general, and fundraising. Program services are the activities that directly relate to the organization’s mission and objectives. Management and general expenses encompass the organization’s administrative costs, while fundraising expenses relate to activities aimed at raising resources to support the organization’s mission.

- Expense Classification: Within each functional category, expenses are further classified by their nature, such as salaries and wages, employee benefits, rent, utilities, office supplies, and professional fees. This classification system allows stakeholders to understand the allocation of resources to different expense types within each functional area.

- Allocation Methodologies: Organizations use various allocation methods to distribute shared or indirect costs across the functional categories. These methods could include square footage for rent allocation, staff time for salary allocation, or the number of financial transactions for accounting fees. The chosen allocation methodologies should be consistently applied and documented in the organization’s accounting policies.

- Total Expenses: The statement calculates the total expenses for each functional category and the organization as a whole. This information helps stakeholders assess the organization’s resource allocation and the proportion of resources dedicated to program services, administration, and fundraising.

Here’s an example of a Statement of Functional Expenses for a church.

Benefits of the Statement of Functional Expenses

- Transparency: The statement provides a clear picture of how an organization allocates its financial resources across various functions and expense types, allowing stakeholders to understand the organization’s priorities and financial management practices.

- Accountability: By offering a detailed breakdown of expenses, the statement demonstrates an organization’s commitment to financial accountability, enabling stakeholders to assess the efficiency and effectiveness of resource utilization.

- Decision-making: The statement serves as a valuable tool for the organization’s management and board members, helping them make informed decisions regarding resource allocation, budgeting, and strategic planning.

- Compliance: For certain nonprofit organizations, presenting a Statement of Functional Expenses is required under the Generally Accepted Accounting Principles (GAAP) and the Financial Accounting Standards Board (FASB) guidelines.

The Statement of Functional Expenses is a critical financial report for nonprofit organizations that provides a detailed overview of their expenses by function and nature. This statement enhances financial transparency, accountability, and informed decision-making, contributing to the organization’s overall financial management and mission fulfillment.

Choosing an Accounting Software

Church accounting software is an essential tool for managing the finances of a religious organization. Choosing the right software can make a significant difference in the efficiency and accuracy of accounting processes. When selecting church accounting software, there are several key factors to consider.

- Ease of Use: The software should be easy to use, even for those who are not familiar with accounting. It should have an intuitive interface and simple navigation.

- Financial Reporting: The software should offer customizable financial reports that provide real-time information on the organization’s financial health. These reports should include balance sheets (statement of financial position), income statements (statement of activities), and other financial data.

- Budgeting and Planning: The software should have tools for creating and tracking budgets, enabling the organization to plan and control expenses.

- Security and Data Backup: The software should have robust security features, such as user permissions and encryption, to protect financial data. It should also have automatic data backup and disaster recovery options.

- Customer Support: The software solution should have comprehensive customer support, including user guides, online resources, and responsive technical support.

- Cost: The cost of the software should be reasonable and within the organization’s budget. It is also important to consider any additional costs, such as upgrades and maintenance fees.

Selecting the right church accounting software can be a significant asset to the financial management of religious organizations. By considering the listed factors, organizations can choose software that meets their specific needs and enables efficient and accurate accounting practices.

ACCOUNTS by Software4NonProfits is one of the top accounting software solutions crafted exclusively for the accounting needs of nonprofits. Embrace effortless financial management with a user-friendly interface, specialized features, and dedicated customer support. Join 1,300 other nonprofits using the software every month.

Outsourcing vs. In-House Accountant

Deciding whether to hire or outsource a church accountant is an important decision that can impact the financial management of religious institutions. There are advantages and disadvantages to both options, and the right choice depends on the organization’s specific needs and circumstances.

Hiring a Church Accountant or Bookkeeper

Hiring a church accountant involves bringing an accountant onboard as a full-time or part-time employee of the organization. The benefits of hiring a church accountant include:

- Full-Time Support: Hiring an accountant as an employee provides the organization with ongoing and consistent financial support. The accountant is dedicated to the organization and can provide in-depth knowledge of the church’s finances and accounting practices.

- Accountability: An in-house accountant is accountable to the organization’s leadership and is more likely to have a vested interest in the success of the organization.

- Control: Hiring an accountant provides the organization with greater control over its accounting processes, policies, and procedures.

- Access to Resources: An in-house accountant can provide the organization with access to resources such as financial software, accounting systems, and databases.

However, hiring a church accountant also has some drawbacks:

- Cost: Hiring an accountant as an employee can be costly. The organization will need to pay for salary, benefits, and overhead costs.

- Training: The organization will need to provide training to the accountant on the organization’s specific accounting practices and procedures.

- Limited Expertise: An in-house accountant may have limited expertise in specific areas, such as sales tax laws or financial planning.

Outsourcing a Church Accountant

Outsourcing a church accountant involves hiring accounting firms or consultants to handle the organization’s financial management. The benefits of outsourcing a church accountant include:

- Cost Savings: Outsourcing can be more cost-effective than hiring a full-time or part-time employee. The organization can pay for services on an as-needed basis.

- Expertise: An outsourced accountant can provide specialized expertise in areas such as tax law, financial planning, and audit preparation.

- Flexibility: Outsourcing provides the organization with flexibility in terms of the scope and duration of services.

- Time Savings: Outsourcing can save the organization time by eliminating the need to manage an employee and perform administrative tasks.

However, outsourcing a church accountant also has some drawbacks:

- Limited Access: An outsourced accountant may not be available for face-to-face meeting. They may also lack a deep understanding of the organization’s culture and values.

- Lack of Accountability: May not be as accountable to the organization’s leadership as an in-house accountant.

- Control: Outsourcing may limit the organization’s control over its accounting processes, policies, and procedures.

- Communication: Communication with an outsourced accountant can be challenging, especially if there are time zone differences or language barriers.

Whether to hire or outsource a church accountant depends on the organization’s specific needs, budget, and circumstances. An in-house accountant provides ongoing support, accountability, and control, but can be costly and may have limited expertise. Outsourcing can be cost-effective and provide specialized expertise but may limit access, accountability, and control. Ultimately, the organization should carefully consider both options and choose what works for them.

Conclusion

Accounting for Churches is an indispensable resource for churches of all sizes seeking to optimize their financial management. By implementing the best practices and strategies detailed in this guide, church leaders can ensure transparency, accuracy, and compliance, all while staying true to their mission and values.

Ultimately, mastering the art of church accounting empowers faith communities to focus on what truly matters: fostering spiritual growth and positively impacting the lives of their members.